[Update: The original piece reported that 48% of passthrough income goes to the top 1%. In fact, it’s much higher than that — 68% goes to the top 1%. This has been corrected below.]

With November 3’s results certified, the election after the election has begun. The race is on to fill outgoing House Speaker Nicholas Mattiello’s spot as the Ocean State’s most powerful politician.

One leading contender is Joseph Shekarchi, a Warwick Democrat who has served as House Majority Leader since 2016. Shekarchi is mobilizing support, capitalizing on his relationships with colleagues and fundraising prowess.

But what’s his in legislative record?

In Rhode Island, the primary vehicle for passing new ideas into law is the annual state budget, a roughly 500-page document that covers public spending, taxation, regulation, social services and more — in short, it includes just about anything legislative leaders want it to include.

As the Speaker’s Number Two in the top-down House of Representatives, Shekarchi has had unique clout to advance his agenda through the state budget. Legislators who back leadership are often able to find a place for their priorities, just as those who oppose leadership are iced out of the process. With outsized influence and many worthy causes to choose from, a legislative leader’s choice of what to fight for says a lot about that lawmaker.

Shekarchi recently made the choice to fight for a big tax loophole for the rich. What should his colleagues make of that?

During the 2020 budget-writing cycle, the Majority Leader championed a measure to help business owners avoid paying federal taxes. His proposal, wedged into the budget and signed into law with the rest of the package in July 2019, was aimed at taxpayers who own passthrough entities — tightly-held companies whose income is taxed at the individual level of the companies’ owners, not the corporate level.

Some passthrough owners, like other wealthy taxpayers, were negatively impacted by the federal $10,000 maximum on state and local tax deductions enacted by the 2017 Tax Cuts and Jobs Act. Shekarchi’s legislation offers a workaround to the federal cap, in effect allowing passthrough business owners to report income related to the entity as corporate income instead of personal income. The change in reporting allows these taxpayers to deduct state and local taxes paid from their federal tax calculation with no limit. While the workaround does not affect state or local government revenue, it does give business owners a big break on their federal taxes.

“I’m working hard to push this bill through,” Shekarchi told GoLocal Providence’s Kate Nagle in March, as General Assembly consideration of the budget was revving up. Shortly after Governor Gina Raimondo signed the final budget in July, Shekarchi told Bill Bartholomew on an episode of the Bartholomewtown Podcast, “I’m proud to say that we have a tax cut in the budget for small business. That’s something that I worked on very hard.”

In Shekarchi’s legislation, the biggest breaks go to those with the highest incomes. But the Majority Leader didn’t sell it that way to colleagues and the public — and that’s part of the problem. Instead, in many op-eds and media appearances about the tax break, Shekarchi touted that his tax change would help struggling mom-and-pops and everyday Rhode Islanders.

The federal cap on state and local tax deductions “affects about 30 percent of Rhode Islanders, and they will see a tax cut on their tax returns next year,” Shekarchi told Bartholomew. “30 percent of Rhode Islanders will see, according to the Pew Institute, a benefit from this. So why not do it?” He told Nagle that his bill “affects about 39 percent of Rhode Islanders.”

A Warwick Beacon op-ed cited similar statistics: “In Rhode Island, 33 percent of filers use [the deduction], and, on average, they claimed $12,434 in 2015, according to research by Pew Charitable Trusts. Rhode Island is one of 19 states where the average SALT credit exceeds the new $10,000 cap.”

In a press release highlighting his legislation, Shekarchi even took a jab at President Donald Trump, a driving force behind the new federal tax law: “Our small businesses are the backbone of our economy, and face enough challenges without being saddled with new tax burdens by President Trump’s tax plan. We’ve found a viable method to help their owners get credit for the taxes they already pay, so their businesses are not disrupted, forced to make cuts to their workforce or worse, to close.”

Rhetoric aside, Shekarchi’s tax law and the Trump tax law largely benefit the same group: the one percent. Let’s break down the Majority Leader’s claims and where they fall short.

First, there’s the proposition that everyday Rhode Islanders were slammed by the federal cap on state and local tax deductions. The Majority Leader is correct that, before the 2017 federal tax law, a third of Rhode Island taxpayers itemized state and local taxes on their federal filings. He appears to be referencing this 2018 issue brief by the Pew Charitable Trusts, which finds that 33 percent of taxpayers claimed the deduction in 2015, and, among those who claimed it, the average deduction was just over $12,000.

But here’s where the wheels start to come off. Shekarchi’s comments imply that one in three taxpayers has been harmed by the cap on state and local deductions, and, in the inverse, one in three “will see … a benefit” from the state-level workaround. This is nowhere near true — and it masks upside-down distributional effects of his legislation.

By and large, Shekarchi’s bill only touches the top one percent. That’s because, to benefit at all from the state-level tax change, one must first owe more than $10,000 in state and local taxes and opt to itemize. People itemizing state and local tax liabilities of this size tend to have high incomes — especially after the 2017 federal expansion of the standard deduction. Rhode Islanders in the bottom 99 percent have been almost universally unharmed by the federal cap, and thus don’t stand to gain from Shekarchi’s workaround. Among Ocean State taxpayers with incomes below $500,000 (the threshold to reach the top one percent in Rhode Island is $467,700, according to the Institute on Taxation and Economic Policy), roughly 50,000 claimed the state and local deduction in 2018. Their average deduction was $7,236, far below the $10,000 ceiling. The $12,434 average deduction Shekarchi cites is driven to such heights by the one percent, not everyday Rhode Islanders.

Then there’s the fact that, to see any direct benefit, one must also own a passthrough business that sees a large influx of cash each year — enough to accrue more than $10,000 in state and local taxes on one’s share of the gain (in addition to tax owings from from real estate and other sources).

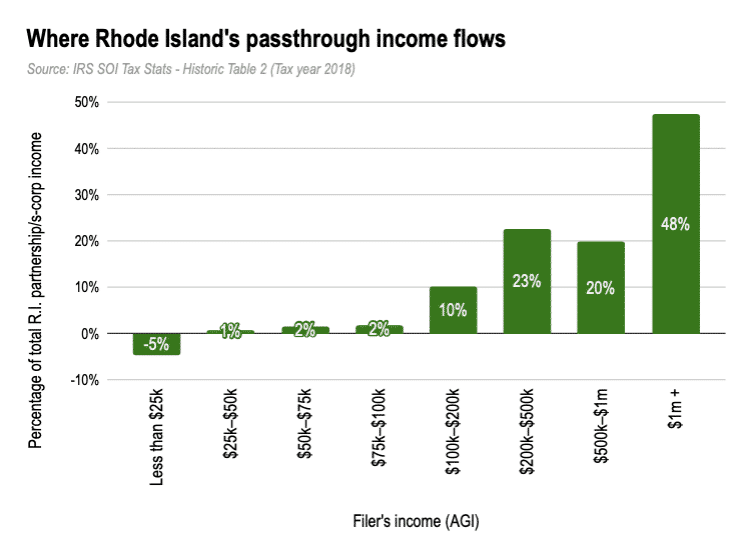

So who receives passthrough corporation income in Rhode Island? You guessed it: the one percent. In 2018, nearly 28,000 Rhode Island taxpayers reported a total of $1.82 billion in income from passthrough entities including partnerships and S corporations. 68 percent — two of every three dollars — flowed to the richest one percent, those with incomes over $500,000. The middle class, meanwhile, reaped far less: Just 14 percent went to individuals with incomes between $50,000 and $200,000.

There’s one more justification Shekarchi offered for his bill: It was needed to help even out the playing field between big business and small business. The 2017 federal tax law slashed the corporate tax rate paid by larger C corporations and less dramatically decreased the personal income tax rates paid by owners of smaller passthrough companies, the argument went. And the state-and-local deduction cap applied to personal income was not applied to corporate income. “The federal government, when they enacted the Trump tax overhaul last year, they gave favorable tax status to C corporations, but not to S corporations and not to small people,” Shekarchi told GoLocal Providence. “So we’ve made some adjustments — or proposed to make some adjustments — in our tax code that would level the playing field.”

But this is not entirely true either. Passthrough companies have historically enjoyed a variety of tax advantages over companies that are taxed separately from their owners — advantages which warp the field in their favor. For instance, a passthrough can use business losses to offset personal income taxes, while C corporation losses can only cancel out income within the corporation. And the Trump tax law did, in fact, cut taxes for passthrough owners: It created a new deduction which reduces the top marginal tax rate on most forms of passthrough income from 39.6 percent to 29.6 percent.

As General Assembly leaders developed the fiscal year 2020 budget, advocates pressed for measures to support Rhode Islanders. Among their ideas: Raising the minimum wage, expanding the earned income tax credit, creating a funding stream for affordable housing, ensuring gender-pay equity, increasing cash support for out-of-work parents, expanding tuition-free higher education to Rhode Island College — the list goes on. None of these made it into the final budget.

From his influential perch, the Majority Leader prioritized a tax loophole for the rich. And to sell the loophole to colleagues and constituents, he employed misleading statistics. Why?

It’s possible Shekarchi was just taking cues from Rhode Island business leaders, and was unaware that he had been led askew by off-the-mark talking points. Or perhaps the Majority Leader’s plan for economic development is more closely aligned with that of Speaker Mattiello: cut social services, cut government, cut taxes and hope job growth follows. Either way, both colleagues and constituents deserve an explanation.

By many accounts, Shekarchi is well-liked and respected by his colleagues. But before he takes the speaker’s gavel, he needs to demonstrate that he will govern in the interest of all Rhode Islanders — not just the one percent.