SUMMARY:

About 40% of Americans struggle to afford their regular prescription medicines - with 1/3 saying they have skipped filling a prescription one or more times, because of the cost. COVID-19 has exacerbated the problem by causing job and health insurance loss and delaying routine care.

Rhode Island policymakers know skyrocketing prescription drug prices must be better controlled.

Unfortunately, they have ignored a key cost driver: Pharmacy Benefit Managers (PBMs).

PBMs such as CVS Caremark, Express Scripts and OptumRx “manage” prescription drug benefits on behalf of insurers and siphon off enormous revenues in the complex non-transparent system that gets drugs from manufacturers to patients.

Other states are doing a much better job monitoring and controlling PBMs and have saved consumers and tax payers hundreds of millions of dollars.

Rhode Island should follow their lead.

To urge RI policymakers to take action, please sign this petition.

A fully annotated version of this piece is available here.

{kind=link}

What are PBMS?

In between most patients and healthcare providers are middlemen health insurers (“payers”) who take money from patients, pay some to healthcare providers, and keep some for themselves. These multiple payers cause the U.S. to spend about twice per capita what other industrialized nations with “single payer” spend for better universal healthcare.

In the middle of payers, patients and pharmacies, there are Pharmacy Benefit Managers (PBMs).

PBMs: Middlemen for middlemen

PBMs are for-profit companies that “manage” prescription drug benefits for more than 266 million Americans on behalf of payers, including private insurers, Medicare Part D drug plans, government employee plans, large employers, and Medicaid Managed Care Organizations (MCOs).

PBMs help payers:

- create a list of covered drugs for plans (“a formulary”);

- manage drug utilization by enrollees (e.g., by setting co-pays, prior authorization policies, etc.);

- reimburse pharmacies for providing the enrollee drugs.

This article will focus on:

- Who Are Pharmacy Benefit Managers (PBMs)

- How PBMs Harm Consumers and Taxpayers

- PBM Oversight in Other States

- Potential Roadblocks to RI Reforms

- How RI Can Rein in PBMs

WHO ARE PHARMACY BENEFIT MANAGERS (PBMS)

PBMs began in the 1970s as small independent middlemen between insurers and pharmacies, taking a set fee for processing claims.

Today, three PBMs control 80% of the market and are part of large vertically integrated conglomerates that include health insurance companies and pharmacies (including “specialty pharmacies”):

- CVSCaremark - 32% market share – parent company: CVS Aetna

- Express Scripts - 24% market share – parent company: Cigna

- OptumRx - 21% market share – parent company: UnitedHealth

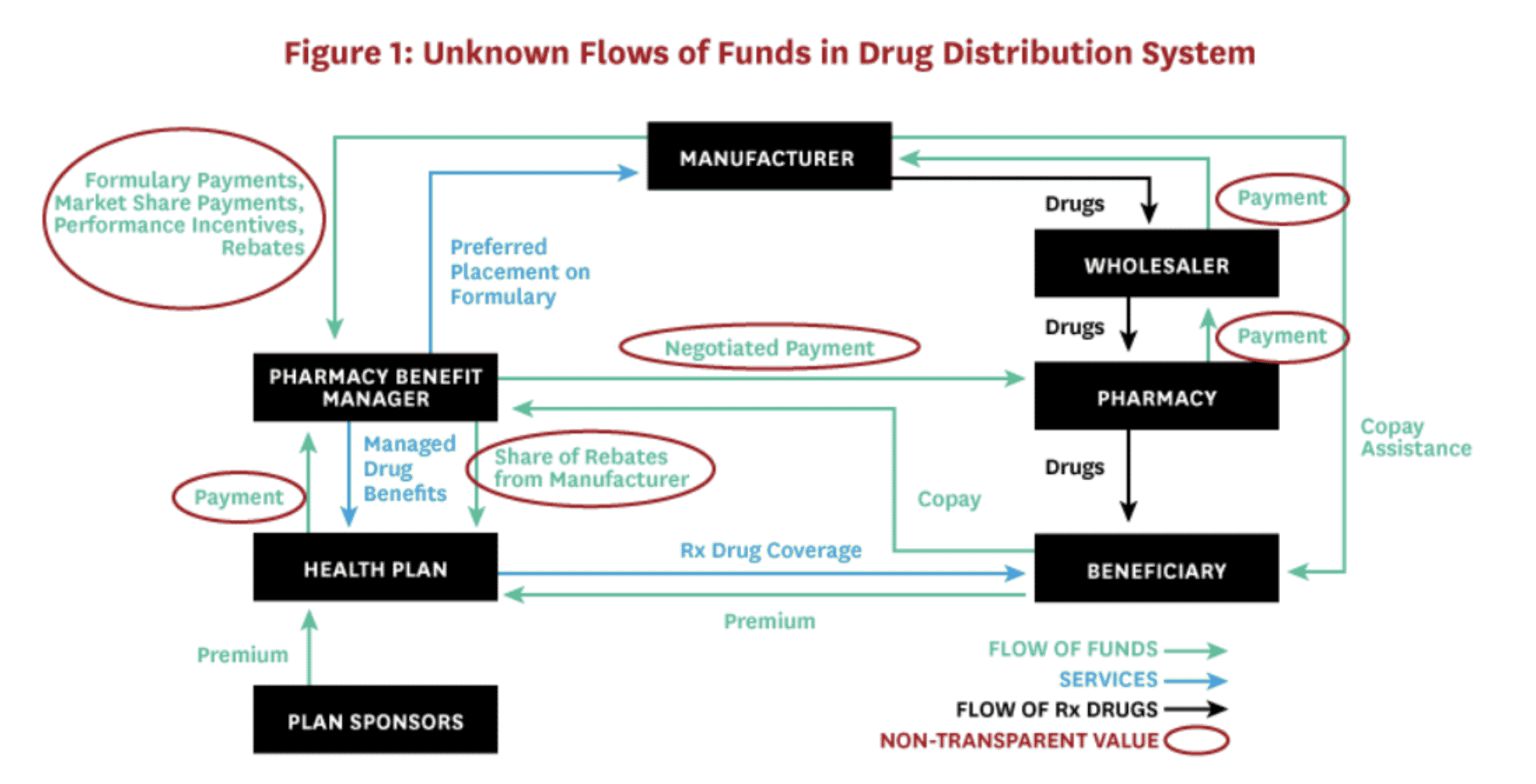

PBMs are also part of a complex non-transparent distribution system that gets drugs from manufacturers to beneficiaries (see Figure 1).

USC Schaeffer Center for Health Policy white paper.

In this system, businesses can keep payments and discounts between themselves confidential, but analyses show that pharmaceutical manufacturers make the most profits for developing and manufacturing prescription drugs AND:

Revenues of top PBM conglomerates exceed those of top pharmaceutical manufacturers.

PBM conglomerates rank 4th (CVS), 5th (UnitedHealth Group) and 13th (Cigna) on the Fortune 500 list ranking largest corporations by revenue.

PBMs drive revenues for their parent companies:

- “CVS Health's Pharmacy Services (PBM) segment will make 46% of $324 Billion in 2021 revenues for the company and remains key to its revenue growth.”

- In 2019, Cigna’s total revenues more than doubled ($14.3 billion to $38.2 billion) and its Express Scripts Holding Co. unit was the “driving force” behind the $22 billion surge.

- UnitedHealth's Optum subsidiaries collected more profit in the fourth quarter of 2019 ($3 billion) than United Healthcare insurance ($2.1 billion).

HOW PBMs HARM CONSUMERS AND TAXPAYERS

1. PBMs get legal kickbacks (“rebates”) from drug manufacturers for putting certain drugs on formularies

When PBMs create a list of covered drugs, they negotiate with drug manufacturers for legal kickbacks (“rebates”) in exchange for giving certain drugs preferred placement on formularies (e.g., Tier 1 with no co-pay, etc.).

Kickbacks are generally illegal under federal law, but PBMs are given a “safe harbor” and a federal rule making PBM rebates illegal has been delayed.

PBMs have a conflict of interest developing formularies because they get more money for shareholders by choosing an expensive drug with a higher rebate than by choosing the most effective or affordable drug for consumers.

Although PBMs pass rebates to insurers (who may be their parent companies) and claim this will result in lower premiums and co-pays, analyses show there is no such trickle down to consumers.

In fact, drug manufacturers cover PBM rebates by raising their list prices for drugs and consumers pay a higher co-pay because they pay a % of the higher list prices.

At $143 billion in 2019, it is estimated that rebates added nearly 30 cents per dollar to the price consumers pay for prescriptions.

2. PBMs overcharge payers (including state Medicaid) and underpay pharmacies because they can keep the difference (“spread”) between what they are paid and how much they reimburse pharmacies

Multiple states have found PBMs problems related to their keeping the “spread.” An Ohio audit, for example, found that in one year, “CVS Caremark and UnitedHealth’s OptumRx PBMs reaped more than $223 million—and made an 8.8% profit—by overcharging Medicaid managed care plans, underpaying pharmacies, and pocketing the difference.”

Ohio found the spread came to $5.70 per prescription across all brand-name and generic drugs and that Ohio could have gotten the same services for $1.90 per prescription or less by switching to a fee-based model – where pharmacies are reimbursed their acquisition cost plus a set administrative fee.

Ohio ordered managed-care plans in the state to terminate PBM spread pricing contracts for 2019

3. PBMs “claw back” and keep excess consumer co-pays

Consumers are often unaware they could have paid less if they had NOT used their insurance (for example, when a co-pay is $10, but the drug price without insurance is $7).

Although consumers should be allowed to recover such overpayments, PBMs are the ones who “claw back” overpayments - and keep them.

A study by researchers at the University of Southern California Schaeffer Center for Health Policy & Economics found that because of PBM claw backs, customers overpaid for their prescriptions 23 percent of the time.

4. PBMs profit from a federal program (“Section 340B”) meant to help low income patients

In 1992, Congress enacted Section 340B of the Public Health Service Act mandating that pharmaceutical manufacturers provide outpatient drugs at significant discounts to certain “covered entities.” 340B’s original purpose was to allow a handful of safety-net hospitals that cared for the poor to obtain drugs at substantially reduced prices.

Changing federal laws caused the number of entities eligible for 340B discounts to explode so that today, there are now about 5,000 covered entities and 20,000 affiliated sites, as well as, “30,000 pharmacy locations - half of the entire U.S. pharmacy industry - now act[ing] as contract pharmacies for the hospitals and other healthcare providers that participate in the 340B program.” 340B discounted drugs make up “more than 8% of the total U.S. drug market and about 16% of the total rebates and discounts that manufacturers provide.”

This large, complex and relatively unknown program is detailed here, but PBM problems generally involve their engaging in “discriminatory reimbursement,” e.g., offering 340B entities lower reimbursement rates than those offered to non-340B entities.

Currently, the federal 340B statute allows PBMs to make significant revenues and not pass money to those Section 340B intended to help.

5. PBM conglomerates own retail, mail order and specialty pharmacies and can work against consumer interests by:

- Setting low reimbursements for their competitors – a cause of local independent pharmacies disappearing.

- Pharmacy Steering – PBMs “steer” customers to pharmacies, including mail order and specialty pharmacies, with whom they are affiliated, e.g., by requiring a higher copay if the patient obtains the drug from a non-affiliated pharmacy.

- Pharmacist gag orders – despite a federal law and a new 2021 Rhode Island law that prohibits PBMs from preventing pharmacists from discussing cheaper options, the consumer still has to ask and may not be told all options.

6. PBMs can hide profits

Reasons for the lack of transparency noted in Figure 1 include:

- PBMs keeping their negotiated discounts and rebates confidential - even from a recent federal Senate committee investigating insulin prices.

- PBMs disguising profits, e.g., as “rebate management fees” and “savings.”

- PBMs controlling their own audits, e.g., by having the right to veto auditors, determine frequency of audits, require auditors to sign “Confidentiality Agreements,” etc.

7. PBM “Utilization Management” can harm patients

PBMs claim to implement “utilization management” strategies on behalf of payers to benefit payers AND consumers. These strategies can include:

- “Prior authorization,” which requires patients to get third-party approval prior to getting the medicine prescribed by their healthcare provider.

- “Step therapy,” also known as “fail-first,” “sequencing,” and “tiering,” which requires patients to start with lower-priced medications before being approved for originally prescribed medications.

- “Non-medical drug switching” which forces patients off their current therapies for no reason other than to save money. “Tactics include increasing out-of-pocket costs, moving treatments to higher cost tiers, or terminating coverage of a particular drug.”

Unfortunately, such utilization management can also harm consumers by making providers spend excessive time on administrative tasks, delaying and discouraging patient care, and adversely affecting clinical outcomes.

PBM Oversight in Other States

Rhode Island has some PBM-related laws and regulations, but other states are more aggressively investigating and reining in PBMs to better protect consumers and tax payers.

A recent Supreme Court case, Rutledge v. PCMA, supports states taking more actions to regulate PBMs.

Some actions other states are taking include:

1. Imposing transparency reporting requirements

27 states with private insurance companies (Managed Care Organizations - MCOs) managing their Medicaid programs reported they will have transparency reporting requirements in place in FY 2020.

For example:

- Texas passed a 2019 law requiring PBMs to report information to the state and discovered, “Since 2016, through a complex rebate and price concession process, the PBM industry in Texas pocketed more than $350 million in revenue, while passing a mere $16 million in savings to enrollees.”

2. Investigating PBMs

Several states have investigated or are currently investigating PBMs.

- Florida: State audit found “prescription markups” by PBMs cost Florida’s Medicaid system $113.3 million in 2020 ($89.6 million in “spread costs”).

- Kentucky: Attorney General investigating PBMs for overcharging the state and discriminating against independent pharmacies after state discovers PBMs kept $123.5 million in spread annually.

- Massachusetts: Investigation found prices charged by PBMs for generic drugs were often “markedly higher” than the actual cost of the drug in both Mass Medicaid Managed Care and Commercial Plans, “contributing to higher health care spending” (e.g., up to 111% more for certain drugs than in fee-for-service state-managed Medicaid program).

- Mississippi: Auditor General is investigating PBMs suspected of overcharging state Medicaid and the Mississippi State and School Employees’ Life and Health Insurance Plan, which covers nearly 200,000 state employees, retirees and their families after audit found PBMs were paid more than $1.1 billion; sometimes as much as $25 million a month.

- Pennsylvania: Auditor General found between 2013 and 2017, the amount that taxpayers paid to PBMs for Medicaid enrollees more than doubled from $1.41 billion to $2.86 billion and is urging greater transparency and more state control.

3. Carving out PBMs from managing Medicaid pharmacy benefits

- Four states reported in 2019 that they generally “carve out” pharmacy benefits from their Medicaid managed care programs (Missouri, West Virginia, Tennessee and Wisconsin) and other states were considering doing so.

- West Virginia “carved out” PBMs, including Express Scripts and CVS, from its Medicaid managed-care program and began running the program as a fee-for-service program - eliminating spreads and reducing administrative fees. It expected to save $30 million a year—about 4 percent of the state Medicaid drug spending. In fact, WV Medicaid saved $54.4 million in its first year and $122 million that used to go to out-of-state PBMs instead went to West Virginia pharmacies in the form of fixed dispensing fees.

- Ohio contracted with a single PBM for Medicaid after undertaking the state audit described above and the State Auditor concluding, “It is now overwhelmingly apparent that PBMs are operating the biggest shell game in modern history, and we are all paying for it."

- Prohibiting spread pricing

- About 17 states reported a spread pricing prohibition would take effect by January 2021 (Figure 3).

- Arkansas: Passed a law, upheld by the Supreme Court, that required all PBMs to reimburse pharmacies at a price equal to or higher than what the pharmacy paid to buy the drug from a wholesaler.

- Maryland: Banned spread pricing after a state Medicaid report found PBMs pocketed “spread” of $72 million annually.

- Ohio: Ended spread pricing contracts with PBMs and switched to a pass-through model following a state audit that found PBM profit accounted for 31.4% ($208.4 million) of the $662.7 million paid by Ohio Medicaid MCOs for generic drugs.

- About 17 states reported a spread pricing prohibition would take effect by January 2021 (Figure 3).

4. Restricting PBM rebates

- Ohio: rebates and discounts must be passed back to the state.

- Maine: required PBMs to pass rebates and other “compensation” to consumers or insurers (who must in turn apply the funds to “offset the premium for covered persons”).

- West Virginia: now handles pharmacy benefits for both state workers and Medicaid recipients through the West Virginia State University of Pharmacy, saving $38 million in its first year.

- About 17 states: have enacted stronger laws requiring PBMs to disclose rebate information.

5. Prohibiting “claw backs”

- About 38 states have prohibited PBM “claw backs.”

6. Prohibiting pharmacy discrimination

- Georgia, Louisiana, Minnesota and Utah have passed legislation banning the practice of “pharmacy steering.”

- Kentucky created an act that requires PBMs to provide greater transparency and “fair and reasonable” reimbursements.

7. Restricting Section 340B reimbursements

- About 11 states: have passed legislation to prohibit PBMs from reimbursing 340B covered entities less than other entities who get their standard reimbursement rate.

8. Limiting “Utilization Management”

- Prior Authorization - 12 states (including RI) have legislation protecting drug classes or categories from using Prior Authorization in some or all circumstances, and most (excluding RI) also apply such statutory limits to Medicaid MCOS.

- Step Therapy - 11 states have passed and many more are considering legislation to limit Step Therapy, e.g., Arkansas became the first state to pass a comprehensive step-therapy ban.

- Non-Medical Drug Switching - Several states have prohibited or introduced bills limiting non-medical switching.

Potential Roadblocks to RI Reforms

1. CVS-Aetna-Caremark

- CVS Caremark is a large Rhode Island-based corporation whose single biggest source of revenue is its PBM business.

- Although the full extent of corporate influence is difficult to discern, it can be significant, and:

- CVS pays lobbyists large sums (e.g., Pharmacy Care Management Association -PCMA, $3,962,000 in 2020) to advocate in RI against PBM reforms.

- CVS contributes to RI elected leaders who have not voted to investigate nor control middlemen payers and PBMs as healthcare cost drivers.

- CVS has threatened to cut RI jobs to influence proposed legislation.

- Since 2010, CVS has secured over $240 million in Rhode Island tax breaks despite apparently cutting its RI workforce from about 12,000 to 3,000 (including getting over $20 million in FY2016 and cutting 247 jobs without notice to the state) and despite taxpayers paying for at least 300 RI CVS employees on Medicaid.

2. The RI Executive Office of Health and Human Services (EOHHS)

- RI EOHHS has advocated for RI Medicaid to be “managed” by private insurance companies - despite lack of evidence that privatizing Medicaid serves consumers and taxpayers better than the fee-for-service state-run Medicaid program previously in place.

- Today, about 90% of RI Medicaid is run by managed care organizations (MCOs): Neighborhood Health Plan of Rhode Island, Tufts Health Plan and United Healthcare Community Plan) who are paid approximately $1.7 billion annually (about 40% state/60% federal funds) - even though the RI Auditor General, since 2009, has flagged inadequate state MCO oversight.

- RI MCO contracts, scheduled to expire in April 2022, are missing PBM oversight and restrictions, e.g., they:

- do not have reporting requirements to identify the amount of PBM spread.

- do not make statutory limitations on prior authorizations also apply to Medicaid managed care PBMs.

3. RI Office of Health Insurance Commissioner

- Rhode Island is the only state in the country to have a separate “Office of Health Insurance Commissioner” (OHIC) whose #1 listed purpose is to “guard the solvency of health insurers.” See RIGL § 42-14.5-2.

- Although OHIC may also seek to protect consumers, it appears to prioritize health insurer economic interests, e.g., raising health insurance premiums during the COVID-19 pandemic.

- OHIC recognizes prescription drug costs are major healthcare cost drivers, however, its analyses fail to consider what role insurers and PBMs play in skyrocketing healthcare costs.

4. RI Health Care Costs Trends Project

- The latest major research effort to study Rhode Island healthcare costs is the RI Health Care Cost Trends Project (“Cost Trends Project”), a “private-public partnership” funded by a $550,000 grant from the Peterson Center on Healthcare (PCH), founded by Pete Peterson, a “power from Wall Street to Washington,” who championed the theory that “entitlement programs” like Medicare, Medicaid and Social Security, would wreck the US economy. PCH-sponsored analyses do not analyze whether middlemen insurers and PBMs could be cost drivers.

- The Cost Trends Project’s goals are to “identify cost and utilization drivers, develop an annual health care cost growth target, and inform system performance improvements.”

- After spending its initial $550,000 grant, the Cost Trends Project has produced analyses that ignore how insurers and PBMs affect health care costs and could not establish an accurate “annual health care cost growth target.”

- A majority of the Cost Trends Project’s steering committee and staff:

- have ties to insurance company or PBM middlemen occupying current or former leadership roles, or

- are employed by organizations that rely heavily on insurer/PBM funding, or

- have a history of producing healthcare cost analyses that fail to analyze middlemen and focus on reining in providers, despite evidence that such policies are ineffective.

What RI Should Do

Rhode Island legislative and executive branch officials should follow the lead of other states more aggressively reining in PBMs, including:

- Require PBMs to disclose information that results in effective ongoing state oversight and control of PBMs.

- Pursue appropriate civil and criminal investigations and actions.

- Carve out PBMs from Medicaid Managed Care Organization (MCO) contracts set to renew in April 2022.

- Restrict Insurer/PBM middlemen unjustified revenues, such as those arising from spread pricing, “claw backs,” “pharmacy steering,” discriminatory reimbursements, manufacturer rebates, and Section 340B transactions.

- Restrict harmful Insurer/PBM utilization management practices, such as, Prior Authorization, Step Therapy and Non-medical Drug Switching.

- Establish an unbiased research group to analyze ALL potential healthcare cost drivers, including private middlemen insurers and PBMs.

WHAT YOU CAN DO

Sign this petition to ask state legislators, OHIC and EOHHS to reform oversight and control over RI PBMs.