We've all been through it. A company we do business with makes a mistake but doesn't come clean, or worse - their error puts you in a bad financial situation. It may seem like an uphill battle, but there several actions you can take to even the playing field, and in many cases get the resolution you deserve. Here, we will run through a real life situation that occurred with TD Bank, but many of the steps can be applied to other types of businesses.

Back in October of 2023, I attempted to pay my TD Bank credit card using their online bill payment feature as I had always done, but this time it did not work. I got a generic "try again later" error when trying to make the payment. So I did, a few hours later. Then the next day. Then a couple of days later. No luck. As my due date approached, I reached out to online banking support to report the problem. They acknowledged the problem and asked me to try the next day and also try it via their app. I opened my TD Bank app and tried to pay that way and surprisingly got the same error. It seemed this was not just a website issue but a pretty big problem with their online payment system altogether.

As my due date come up, I reached out again explaining that I could not pay my bill and would need them to waive any late fees or interest that would arise as a result of this. Now, you may be wondering why I did not just mail them a check and there is a very good reason for this: because they don't mail me a statement. As we all know, many large businesses want to do away with the cost of mailing statements to customers. In TD Bank's case, they penalize those who want a paper statement with a monthly fee. So, because TD Bank won't mail me a statement without assessing a fee, I applied the same logic and refused to mail them payment unless they paid me a fee (to nobody's surprise, they were not willing to do this).

A month went by and the issue was still not resolved. That's right, a giant bank like TD Bank had its system to make online credit card payments go down for over a month. If you think that's bad, Subway's website has been unable to complete online orders for most customers for the past year and the sandwich folks not only have not fixed the issue but seem to be unaware of it. But we'll save our tales of incompetently managed big businesses for another piece down the road. Back to TD Bank, I now had late fees and interest applied to my "late" payment. I decided for my mental health to stop worrying about the problem and assumed TD Bank would make it right in the end. I was wrong.

Another month went by and still their online payment system produced errors, different errors than before, but still left me unable to give them my money. The bank's customer service team responded to my pleas that once they received payment from me, they would waive the late fees and interest. After nearly 90 days, their system was fixed and I immediately paid my balance, minus the fees they tacked on. I had no intention of paying the fees because after all, it was not my fault that payment was late.

Then I noticed that TD Bank was reporting my late payment to the credit bureaus, sinking my credit score by over 130 points. Now we had a problem - or rather, now they had a problem. A quick side note about me: I am the crazy type of person that will spend $1,000 to make a large company fix a $25 mistake. I am the type of person that will get the local news to do a story even after the town promised to fix the problem, and in other cases until they fix the problem. Why? Because when large organizations that hold power - be it the government or a big bank - screw the regular guy, there must be accountability so that they [hopefully] take steps to ensure it does not happen again. This accountability takes two forms: compensating you for fees they shouldn't have charged and wasting their time. Here is how I got my resolution and the steps you can take when faced with the same dilemma:

- Giving Them a Chance. Write to the company in question. Tell them what happened, what you want, and why it is in their best interest to resolve the problem. In my case, I wrote to TD Bank using their online messaging function explaining the bill payment issue and that I was sure they would prefer to avoid complaints being filed with their government regulators. Unfortunately, this went to contracted service reps who couldn't have cared less and the response I received was of no help. But you may be surprised, this can sometimes yield positive results.

- Giving Them a Final Chance. Ensure that you have reached out to all relevant points of contact. Sometimes the corporate office may not be of help but the local office can fix your issue. I mailed a letter to the bank's corporate address and my local branch, reiterating the issue and my preferred resolution, which was to waive all assessed fees that resulted from the late payment and fix my credit report. I gave them a deadline to respond within two weeks, after which I would have no choice but to file complaints with the CFPB and their banking regulator. Surprisingly, I did not even hear back from my local branch. But in the past, I've had decent luck with this step. By the way, there is a great service you can use to do much of the legwork of this step for you called JusticeDirect which will write you the letter for free and send it certified for a reasonable fee.

- Complaint Bombing, Part 1. These are very important steps because not only do they often bring a resolution, but they require the company to spend real human labor to review and respond to the complaint. This is important because big businesses know that time is money, and the more of their time you waste, the more money they must spend. My first complaint, as promised, was to the Consumer Financial Protection Bureau (CFPB), one of the few government entities that exists solely to help the powerless fight back against big business (but only financial entities). The CFPB took action and demanded a response from TD Bank. The bank responded that they would waive the late fees but not the interest, claiming that the situation was "not caused by bank error". While it is not common for banks to outright lie to the CFPB in their response, it does happen. My complaint with the CFPB only centered around the interest and late fees. I did not mention the erroneous credit reporting and I'll explain why in step 4.

- Complaint Bombing, Part 2: Carpet Bombing. Now that I knew TD Bank was going to dig its heels in I moved to the next phase: carpet bombing the complaints. This is when you file complaints with all other regulators and business watchdogs simultaneously, which both overwhelms the company with an onslaught of complaints that must be responded to and puts them on notice that the situation is serious and must be addressed. I filed complaints with the RI Attorney General's Consumer Complaint Division, the RI Better Business Bureau (BBB), the Office of the Comptroller of the Currency, all three major credit bureaus, and the CFPB - this time about the false credit reporting, so it appeared as two separate complaints. The entire process of this step took about 30 minutes.

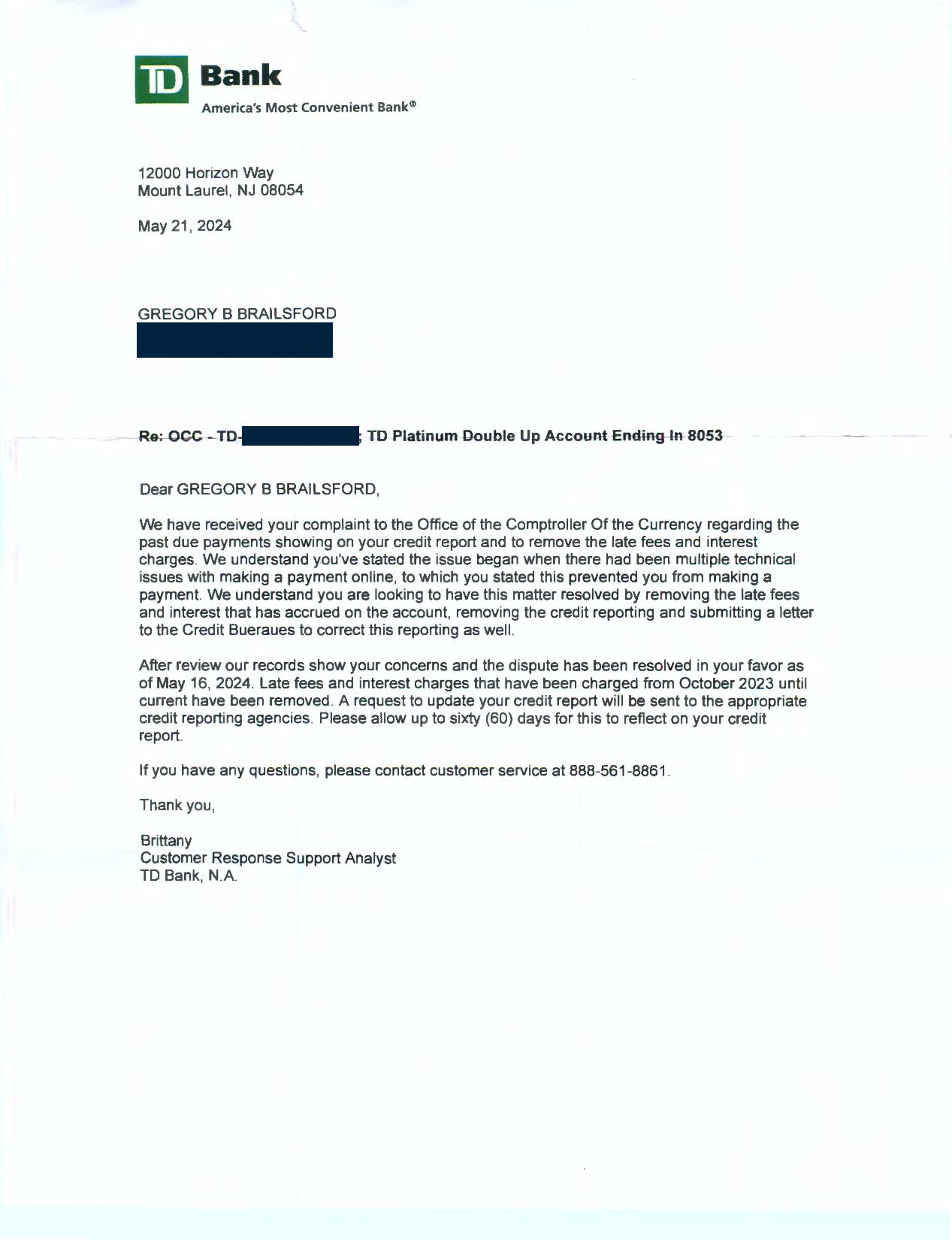

I was curious to see which entity would trigger a resolution. They first responded to the CFPB complaint reiterating their stance that this was my problem and they would do nothing to resolve it. I was then notified by the credit bureaus that they were researching my complaint, which generally involves them asking the company to review and confirm the negative reporting. Then, I received the following letter in the mail:

This letter was eventually followed by responses from the BBB and RI Attorney General, with TD Bank indicating that they previously responded to my complaint with the OCC and had resolved the matter in my favor.

In total, I spent roughly an hour and a half researching, writing up the complaints, and scanning evidence. In return, I got all of the fees/interest waived and all of the negative reporting removed from my credit report. While not everyone may wish to go through the motions that were necessary to resolve a complaint of this nature, it is helpful to know that there are techniques for dealing with corporate bullies. I do not condone this method if you are legitimately at fault and want a bank or other business to fix a problem they did not cause, but if they did you wrong, there are both government agencies and advocate organizations available to help.

Notes: Your results will vary not only with the organization/agency you complain to but also the company you are complaining about. For example, companies like Facebook and Tesla have dozens and perhaps hundreds of complaints on file with the RI Attorney General's Office. They generally do not respond and the AG's office to date has offered little recourse. However, Tesla is very sensitive to complaints filed with the BBB and I have witnessed them swiftly resolve issues when a complaint is filed with the BBB. My complaint to the OCC was the first time I had done so. Be aware that banks and credit unions are not all regulated by the same federal government entity. For example, credit unions answer to the NCUA, rather than the OCC. You can find your bank's regulator at the FFIEC website.